Find out what boat loans are available with a 725 credit score. Learn the things you can do to get a low interest loan and discover how to improve your credit score of 725

Your credit score is what largely determines whether you get credit or not and if the interest rates offered to you will be high or low. A credit score is a number that is calculated from the information contained in your credit report using a mathematical algorithm. The resulting number has three digits and ranges from 300 to 850.The information in the credit report is collected from the credit bureaus Transunion, Experian, and Equifax.

The credit scoring system was introduced in 1989 by Fair, Isaac, and Company, currently known as FICO. Since then, the FICO model has been adopted by a majority of credit grantors and banks.

According to FICO, 90% of the most reputable and respected lenders today are making decisions based on this credit scoring system.

The following companies are the most popular companies that that measure credit scores: FICO, VantageScore, PLUS Score, TransUnion, Experian National Equivalency Score, Equifax, CreditXpert, and ScoreSense.

Credit scores are mostly used when obtaining loans, such as student loans, personal loans, car loans, small business loan and more. Landlords use credit score to determine if you can afford to rent an apartment. Insurance companies use it to determine how much to charge for coverage. Even some cell phone and utility companies use credit scores. It is used by banks, credit grantors, retailers, landlords and various types of lenders to determine how creditworthy you are.

Having good credit means that you will get any financing you need or rent any apartment you want. And when it comes to interest, you will be offered the lowest interest rates. On the other hand, having a bad credit score means that you will be denied different types of credit. Lenders will see you as a very risky borrower and will most likely not approve your loan application. Even some landlords will deny you a lease if your credit score is bad.

Boat loans with a 725 credit score

The opportunities of getting a boat loan with a 725 credit score are high. Boat loans are available include;

Sea Dream Finance and Insurance

They offer finance on amounts up to $60,000. The loan terms go for about 12 years. They offer to finance with simple interest with no pre-payment penalties. The interest rate also varies depending on the amount. The minimum down payment required is 10% and above. Another condition is that the boats should not be older than 15 years. The minimum credit score is also 550 and the debt to income ratio should not exceed 45%.

Lending Tree

The credit score required for one to get a low-interest loan is 725. The life cycles for loans on boats are long and therefore have lower monthly payments. The down payment percentage ranges from 10-20%.

BoatUS

It works with marine lenders to offer competitive boat loans. The minimum credit score considered is 680 with no credit issues such as foreclosures or bankruptcy. A decision on the application is made after 2 to 4 business days and cash is disbursed after 1-2 business days. The rates vary on the loan amounts and they range from 7.49% to 4.62%. The smaller the amount, the higher the interest rate. The monthly payments and down payment also vary.

How is my 725 credit score calculated?

Lenders need to judge if you're a credit-worthy individual before they give you a loan or whatever financing you need. That is where your credit comes in handy. Most lenders look at your FICO score, since it is the most widely used credit score, to determine your credit-worthiness. The specifics of how FICO calculate the score are not known, but it all boils down to the information on your credit report. Your credit report is made up of the following components: payment history (35%), the amount owed (30%), the length of credit history (15%), new credit (10%), and types of credit used (10%).

Payment History

This is one of the essential components, and it accounts for 35% of your credit score. It shows lenders that you have the ability to pay your bills on time. It digs deeper into your payment history to see if any past problems exist, such as delinquency, bankruptcy, and collections. It also looks into the scope of the problems and the resolution time. Your score will be impacted negatively if you have too many problems with your payment history.

Amount Owed

The amount owed is another major component and accounts for 30% of your credit score. This part looks at what you still owe lenders by looking at the types of accounts and the number of accounts in your name. Needless to say that if you owe too many people a lot of money and have too many accounts in your name, your credit score will be negatively affected because this component focuses on your current financial situation the most.

Length of Credit History

A good credit history that spans years will signal to lenders that you are a sound investment compared to someone with a history of missing payments. If you've never missed a payment in over ten years, it counts as a plus when calculating your credit score. This component accounts for 15% of your credit score.

New Credit

If you are always getting credit (accumulating a pile of debt in the process), it must mean you have a lot of financial pressures that are compelling you to do so. Your credit score gets negatively affected every time you apply for new credit, and this component accounts for 10% of your credit score.

Type of Credit Used

This component of the credit score accounts for 10%. Basically, for each credit card you own, your credit score takes a hit. Someone with a lot of credit cards is more of a high-risk borrower than someone with only one.

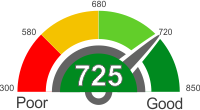

Explanation of credit score ranges

When it comes to purchasing something that requires borrowing money, your credit score is the three-digit number that tells lenders if you're a worthy investment or not. Whether you are applying for a mortgage, home loan, car loan or boat loan, lenders will make a decision after looking at your credit score and other information. The higher your credit score is, the more chances you have at obtaining any loan you want at affordable interest rates (the opposite being true for low credit scores).

300 to 580

A credit score of 580 and below is poor credit, and approximately 61% of people with credit scores are in this range. Credit problems or bankruptcy can lead to a credit score being this low. And if you're in this range, you will find it tough to get financing or loans at all. If you do get them, the rates might not be affordable. Since people in this range are high-risk lenders, the chances of missing or failing to make payments in future (become delinquent) are high. Rebuilding your credit when it is this low will take some time, but it is worthwhile if you want to take advantage of the kind of low interest rates that the higher credit scores get.

581 to 680

Credit scores within this range are above average and count as fair. Approximately 28% of people who have credit scores fall within this range. If you are in this range, you are considered to be a high-risk borrower and will pay interest rates that are slightly higher when you try to obtain financing or loans. The chances of you becoming delinquent in future are also high.

680 to 720

Borrowers in this range are considered to have a good credit score, and they make up approximately 8% of the population of people with credit scores. Your application for financing and loans are considered to be "acceptable," and you have a good chance of getting affordable rates when you apply for loans. There is a high chance of borrowers in the 680 to 720 range to become delinquent in future.

721 to 850

Credit scores in this range are considered to be excellent, and approximately 3% of people with credit scores are in this range. If you have a credit score that falls within this range, you won't find it hard to acquire loans, and you will get much lower rates. There is a high probability of borrows in the 721 to 850 range to become highly delinquent in future.

What does it mean to have a 725 credit score

A 725 credit score is considered good. It qualifies one in the prime group. The people in the category are considered diligent with less than 30% credit utilization. The chances for approval on loans and credit cards are excellent. Also, the interest rate and other terms are average and manageable. The types of loans available include;

FHA loans

These loans require a minimum down payment of 3.5% of the appraised value. The loans are used for property acquisition or financing. Other requirements are credible documents such as social security and financial records. Also considered id the credit to debt ratio which should be low.

Mortgage re-finance

The loans available start at $40,000. Some companies do not have a set minimum and maximum limit. The interest rates range from 3-5% if all necessary documents are provided. The refinance money may be used for paying off other loans, home remodeling, medical or education expenses. However, some lenders restrict the use to a specific use. Some specify that

Personal loans

The personal loans available come with an interest rate starting at 5.99%. Some lenders also charge an origination fee. However, the process of getting personal loans is fast. Individuals with this score often get offers on unsecured loans with no collateral. The amounts given may be used for making improvements to the home, credit card debt or vacation.

Things you can do to improve your credit score of 725

Setup payment reminders

A factor that significantly affects the credit score is making payments on time. Many bureaus give promptness a great priority. To make payments on time, you can ask the lender to help. The lender may help by sending reminders to make payments. They can be in the form of phone calls, emails or texts. It would be much better if there is an automated system in place to remind you to make the payments.

Making payments on time helps you to maintain a good credit score. It is important to keep up with the habit. It is advisable to set reminders that will trigger you to make the payments. You can request your lender to send automated reminders via phone, email, or text.

Get current and stay current

Current credit records are more important than historical information. It is therefore important to maintain a consistent and good record to maintain and improve your credit score. Consistency is when you make the necessary payments as agreed during the duration of the loan. In doing this, the removal of the previous history will not significantly impact the credit score since the practice of payment is uniform. Confidence by the lenders is instilled through regular practice.

A credit score within this range is great. It is crucial to inform the lenders and credit bureaus of your credit worthiness. A good reflection is through current payment history made promptly. In the case of a previous bad credit score, you can remove the records by increasing the current good record. Focus on your current situation and ensure nothing affects the good record. The current financial records have a greater stake when calculating the credit score than the old ones.

Become an authorized user

One can improve their credit score by authorization. This is where you get authorized on a credit card belonging to a person with a good credit record. You get authorized as a user on that account. The good record of prompt payments, consistency and compliance reflects on your record improving your credit score.

Authorization in most cases improves the score to an excellent one. Individuals with a very good payment history can let you be an authorized user and help you get an excellent score.

Keep balances low on credit cards

When you have large amounts of outstanding balances on your credit cards, the credit score might be negatively affected. It is okay to have debt, what is important is making the amount low to avoid any adverse effects on your account.

How you conduct your financial transactions tells a lot especially to the credit bureaus. Not utilizing the credit card fully is one good practice to adopt. An ideal percentage is below 30%. The small spending shows responsibility and that you are not overspending because you can.

Check if you linked your account to others

People link their cards with friends and family. Linking to an individual who has a bad credit score harms your financial record. It is necessary to cut off links with people who might bring your credit down. Before embarking on such a mission, ensure that the person you are connecting to has a consistent record.

It takes hard work to maintain a good credit record in this range. Keeping the good record is imperative. When linking your account to other people, ensure their credit history and financial transactions will not negatively affect your score. Also, you may get linked without knowing. Regularly check your records to ensure edits when it happens.